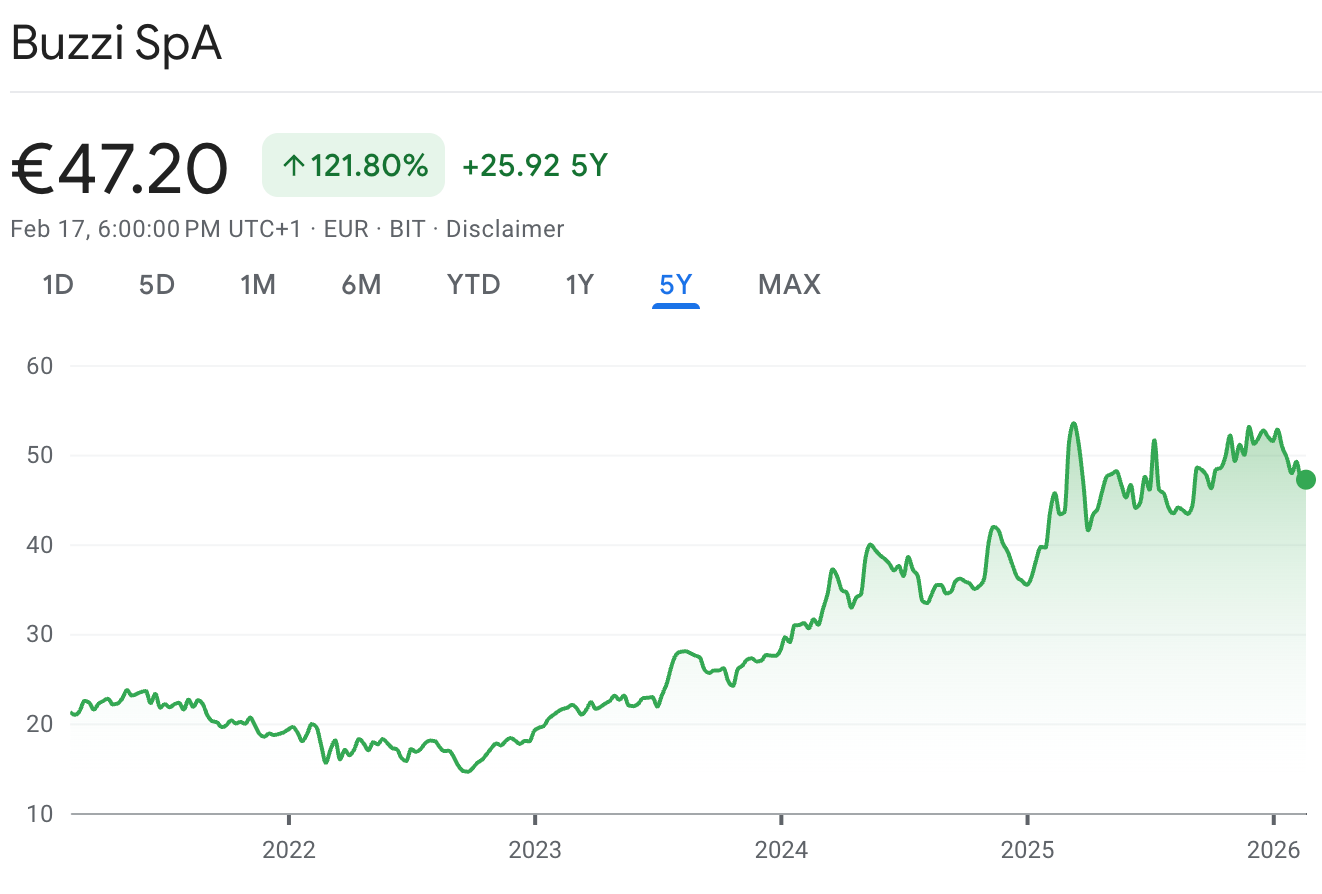

BUZZI S.P.A ($BZU.MI)

The 1B fortress you’ll wish you owned when the sunshine turns to rain.

📊 This thesis has an interactive version → 10 slides, live charts, valuation scenarios and six layers of analyst commentary you won't find in the text below. If you're the type who thinks in visuals, start there.

Link at the end.👇👇.

1. Executive Summary: Investment Case

On the screen, Buzzi looks like a standard Italian cement maker. It’s not. Most of its EBITDA actually comes from dollars in Texas and the Midwest, but the market ignores that. It sees the Milan listing and applies a massive discount. You’re essentially buying US infrastructure assets at a European price.

It’s tempting to compare Buzzi to pure US peers like Eagle Materials, but that’s a trap. Eagle is a different animal pure-play, highly efficient, and aggressive with capital. Buzzi is a slower, family-run business with European baggage and a "lazy" balance sheet. However, even after you apply a heavy "governance tax" and account for the carbon costs in Europe, the gap is hard to ignore. Trading at 6x EBITDA while owning those US kilns doesn't make sense, even for a conservative Italian firm. In the following sections, we’ll break down the business to understand exactly why the market is pricing it this way and whether the current discount offers a real margin of safety or if it’s just a justified 'trap'.

Current Situation

However, the 7.0% drop in US sales needs context. It isn’t just a “soft” housing market; it’s the weight of high interest rates.

Rates Hit: High borrowing costs have frozen residential starts and started to stall commercial projects.

Infrastructure Floor: Public spending on roads and bridges is the only thing keeping volumes from falling off a cliff.

Price over Volume: They managed to stay profitable by hiking prices. It worked for 2025, but this is a defensive play. You can’t squeeze customers forever, especially when the high “price umbrella” is starting to make independent imports look attractive again.

We’re looking at a company that’s successfully defending its ground, but the growth story in the US has clearly hit a plateau. They’re making more money per bag, but they’re selling fewer bags.

The “Italian Discount” So, why is it so cheap? The market isn’t lazy; it sees specific risks that justify this valuation gap. Essentially, there are three clear reasons why investors apply this discount.

First, strictly speaking, it’s about Governance and Cash. The Buzzi family controls the voting rights and runs the company with extreme caution. They prioritize safety over returns. The latest numbers confirm this: they are now sitting on a massive €1.13 billion net cash position. Instead of buying back shares aggressively to close the valuation gap, they just let the cash pile up. Then there is the Russia Problem. They haven’t fully exited the country. This creates a persistent reputational issue and keeps many institutional funds away. Finally, the Green Bill. The industry faces mandatory decarbonization costs. Upgrading kilns for carbon capture is a requirement to operate in the 2030s. That capital expenditure will necessarily depress the free cash flow available for dividends in the coming years.

Value Trap Check Skeptics call Buzzi a “value trap.” They argue that holding over €1 billion in the bank earning 3% interest, while industrial inflation is higher, is mathematically inefficient. It drags down the Return on Equity (ROE). And the critics are right. This capital allocation is lazy. But this isn’t a mistake; it’s a feature of the family’s strategy. They run this company to survive the next 50 years, not to pump the stock price for the next quarter.

Here is the trade-off: You are accepting a lower ROE in exchange for virtually zero bankruptcy risk. The thesis isn’t that they will suddenly change and become aggressive with buybacks. The thesis is that buying prime US assets at 5x EBITDA provides a margin of safety so wide that you make money even with this inefficient capital allocation. You aren’t paying for a catalyst; you are paying for a floor.

2. BUSINESS AUTOPSY: Turning Rock into Cash

This business is simple. Buzzi takes limestone out of the ground, cooks it, and grinds it into powder. That’s it.

They own the quarries. This is step one. If you don’t own the rock, you are just a middleman. They blast the raw material, crush it, and feed it into a massive rotating kiln. This kiln runs 24/7 at temperatures hotter than a volcano (1450°C) to trigger a chemical reaction. This process eats energy, coal, gas, waste tires, or plastic. The result is a hard nodule called “clinker.” They grind this clinker with gypsum, and you get cement.

How They Get Paid They sell in two main ways:

First, Pure Cement (The High Margin). They sell it in bulk silos or bags to construction companies. This is where the real money is. The barriers to entry are massive because you can’t just open a new quarry or build a kiln today without fighting regulators for ten years.

Second, they sell Ready-Mix Concrete (The Volume Channel). They mix their own cement with sand, water, and stones to make liquid concrete (what you see in the spinning trucks). The margins here are very low; it’s basically a commodity. But Buzzi needs this division because it guarantees a customer for their cement plants. It locks in the volume.

The Geographic Deception

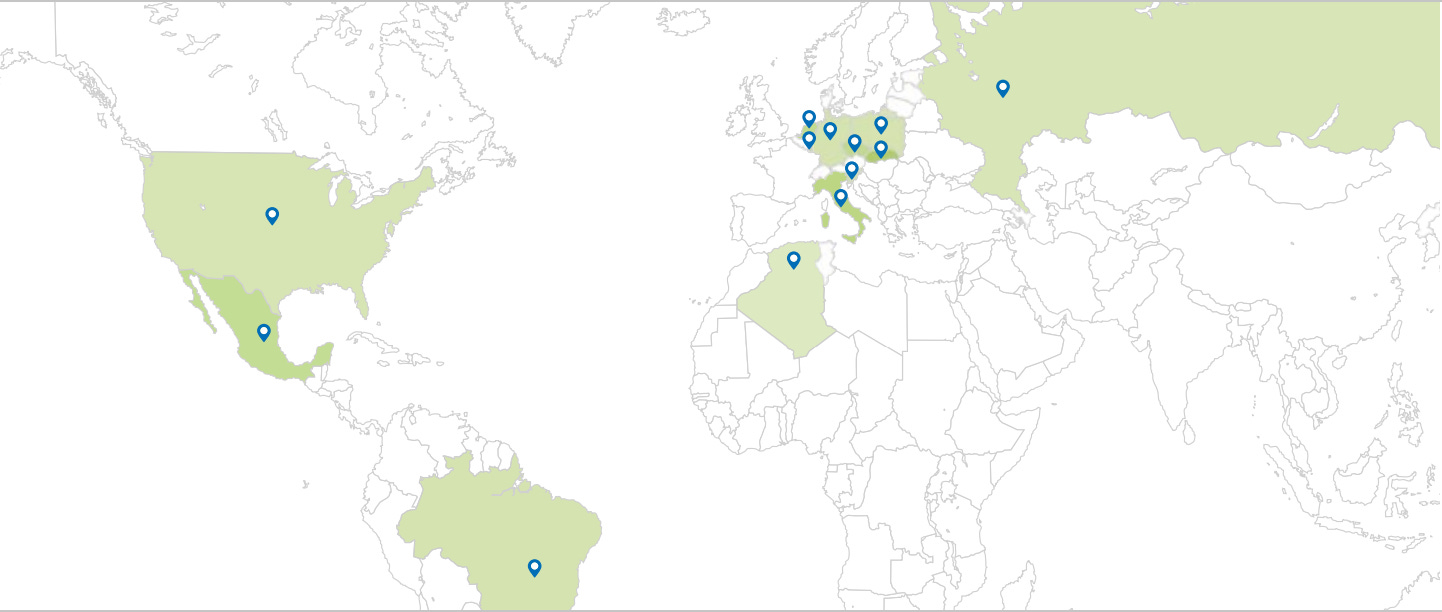

You have to ignore the consolidated revenue line. It creates a false picture. On paper, Buzzi looks like a balanced transatlantic group. But sales don’t pay dividends; EBITDA does. When you look at the profit pool, the reality shifts. They operate in 14 countries, but the weight is not equal.

The US is the engine. It’s about 58% of the total EBITDA. That’s where the actual cash is made. Central Europe (Germany and Lux) follows with 14%, and Italy, the home base, only accounts for 13%. The rest of Eastern Europe (Poland and Czechia) makes up the remaining 15%.👇

European Core: They dominate in Italy and Germany, but they also have strong positions in Poland, the Czech Republic, and Ukraine. These are stable markets dominated by CO2 regulation.

Emerging Growth: Don’t forget Mexico and Brazil. These are high-growth markets where they operate through joint ventures that provide steady dividends.

US & The River Logic Now, let’s look at the real cash machine: The United States. The US division generates the bulk of the group’s EBITDA, although the 2025 results show this engine is cooling down (sales dropped 7%). You are analyzing a company where the cost base is largely in Euros, but the profit is in Dollars.

Why do they win in the US? Logistics. Cement is cheap but heavy. If you move it by truck, you lose money after 200 miles. Logistics are the biggest cost in this industry. Buzzi wins because of the Mississippi River. They own a network of terminals that allows them to float cement on barges from their massive plant in Selma, Missouri, down to Texas or up from New Orleans. River transport is infinitely cheaper than the road or rail transport their competitors use. This physical advantage protects their margin against peers. They don’t just have a better product; they have a cheaper way to move it.

Note: The Limits of the "Moat" Don't confuse a structural advantage with immunity. Despite this river advantage, US margins dropped from 30% to 25% in 2025. This happens because of Operating Leverage. Cement plants have huge fixed costs. Whether you produce 1 million tons or 800k tons, the kiln costs roughly the same to run. So, when volumes drop 7% like they did this year, the profit margin contracts automatically. The river advantage means Buzzi is still more profitable than a competitor using rail, but it doesn't stop the margin from falling when demand dries up. It protects the relative spread, not the absolute number.

Strategy: Price Over Volume

Management behavior is shifting. In the 2023-2024 period, they sacrificed market share to push price increases. That worked when inflation was high. But the 2025 numbers show that strategy has hit a ceiling. In the US, prices actually declined slightly in the final months. The "infinite pricing power" thesis is over for now. Consequently, they are pivoting back to inorganic growth. The acquisition of Gulf Cement (UAE) shows they are buying volume to offset the organic decline in the US. In Europe, the strategy remains defensive: it’s about CO2 management. They use their carbon allowances as a barrier to entry. No new competitor can afford the credits to enter the market, effectively turning these regions into closed oligopolies.

3. COMPETITIVE LANDSCAPE & THREATS

Cement is a local business, but the major players are global. Buzzi does not have a monopoly. They compete for every dollar of EBITDA against giants like Holcim and Heidelberg, as well as aggressive local importers.

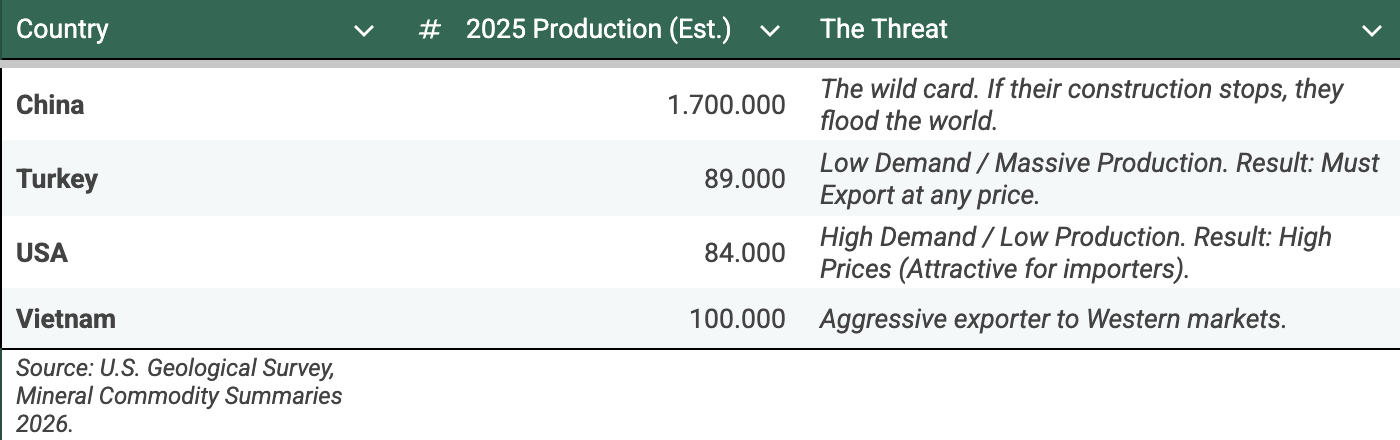

The US market used to be protected, but that has changed. The high margins attracted new players. In the past, Buzzi controlled the import terminals, so they controlled the supply. Now, independent importers are disrupting the status quo. The US Geological Survey (February 2026) confirmed this shift, reporting that "a Turkey-based company opened a new grey cement grinding plant in Texas" just last October. This explains why prices in Texas were flat last year: new, cheap supply is flooding the market right in Buzzi’s local area.

Pietro Buzzi has been very clear about this. The strategy of "price over volume" is paused. With capacity utilization dropping below 100%, Buzzi won’t push aggressive price hikes anymore. If they do, they lose volume to these importers. In a high-fixed-cost industry, losing volume destroys profitability, so they are choosing to protect their market share instead.

There's also a risk with their biggest customer. Quikrete represents about 6% of Buzzi's US sales. If Quikrete finishes buying Summit Materials, they'll become a competitor instead of just a client. This means Buzzi's biggest buyer would have its own factories and wouldn't need to buy as much from them. It's too early to know the exact financial impact, but it definitely puts pressure on US margins.

Quikrete Risk: A Customer Turning into a Rival We have to be realistic about the situation with Quikrete (roughly 6% of sales). If Quikrete finalizes the deal to buy a major producer like Summit Materials, they transform from a client into a competitor. This is a tangible risk. It creates a messy dynamic where your biggest buyer suddenly has their own factories and doesn't need you as much. In the short term, this could leave a volume hole that Buzzi has to fill by fighting for smaller, less profitable clients. It puts real pressure on US margins.

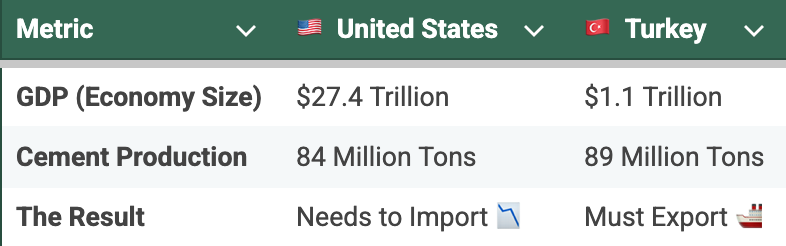

The Great Imbalance: To understand why this happens, look at the supply and demand imbalance. The US economy is huge ($27 trillion GDP), but Turkey’s economy is much smaller (around $1 trillion). Despite this, Turkey produces more cement than the entire United States.

Here is the problem: despite being 27 times smaller economically, Turkey produces more cement than the entire United States.

This creates a structural surplus. Turkey produces way more than it can consume. Since they can't store clinker forever, they are forced to export it to keep their kilns running. Naturally, they look for markets with high prices and strong currency. The US is the perfect target. This hurts Buzzi because if a Turkish ship arrives in Houston selling cement 20% cheaper (because they are desperate for volume and don't pay Carbon Taxes), Buzzi can't raise prices. The customer will just switch to the imported material.

The UAE Move: The Strategic Hedge Buzzi is reacting to this pressure. The acquisition of Gulf Cement Company in the UAE (Ras Al Khaimah) is not just about growth; it is a defensive hedge. Instead of trying to fight cheap imports with expensive local production, Buzzi is joining the game. They now own a low-cost source. They can produce cheap clinker in the UAE, where energy is cheap and regulations are looser, and ship it directly to their Houston terminal. It turns a supply vulnerability into a cost advantage. If the market becomes an import game, Buzzi is now equipped to play it.

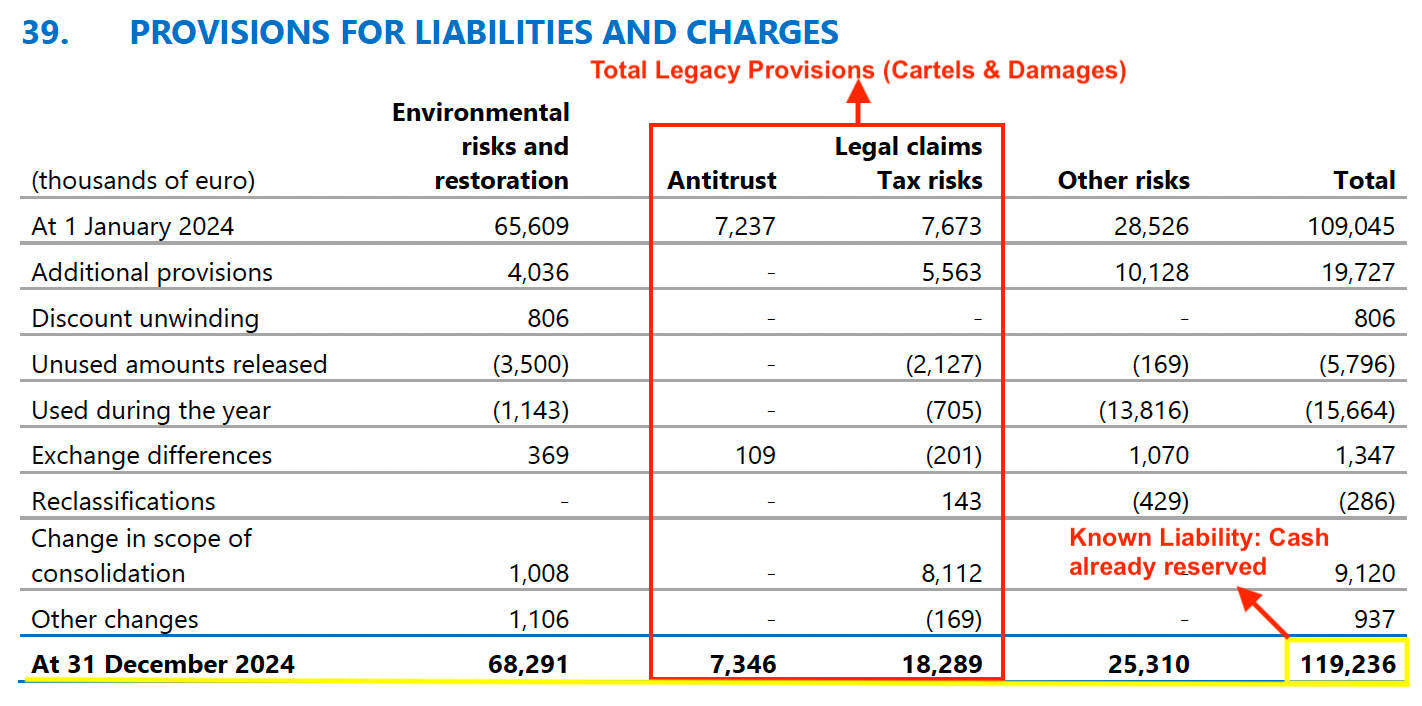

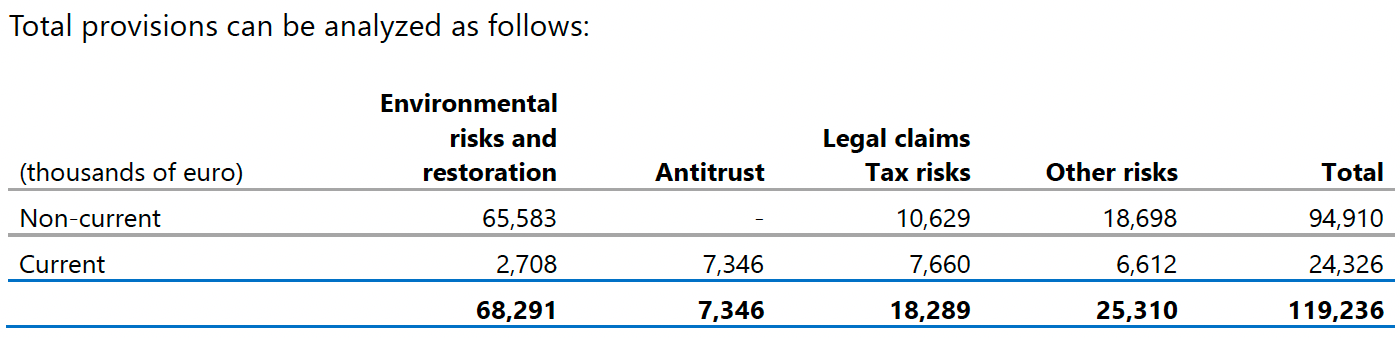

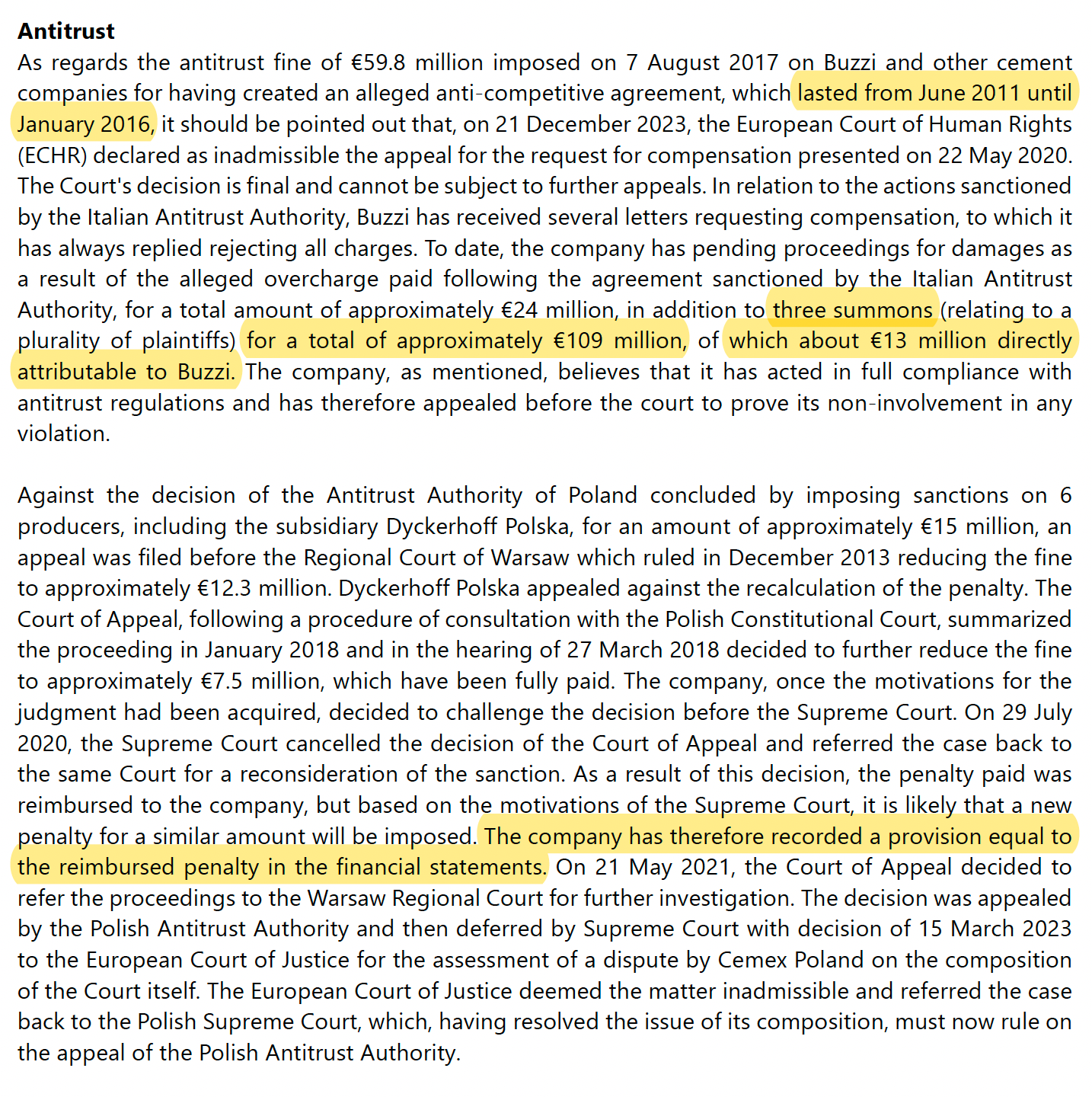

Note: Cleaning up the Balance Sheet Risks: Finally, let's look at the "Provisions" section in the report. You will see big numbers for Legal and Environmental risks. It’s important to understand what these actually are so you don't overestimate the threat.

The Environmental Provision (€68.3M): This is the largest number in the table, but it is not a fine. As Buzzi owns the quarries, they have a legal obligation to restore the land when they finish extracting the rock. This is an Asset Retirement Obligation. If you look closely at the table, €65.6 million is classified as “Non-current”. This means Buzzi doesn’t have to pay this tomorrow. It is a technical debt that will be paid slowly over the next 10 or 20 years as quarries close. Regarding the specific legal issue in Augusta (Sicily), the courts have limited Buzzi’s liability, so the company only holds about €1.5 million for that specific case.

The Antitrust & Legal Claims: The headline number of "€109 million" in civil claims can look alarming, but it doesn’t break the thesis. In these lawsuits, plaintiffs always start with a maximum theoretical figure as a negotiation tactic. The report shows that the portion directly linked to Buzzi is actually closer to €13 million. Since the main fines regarding the 2011-2016 investigation were already paid, the remaining risk is covered by the provisions you see in the table.

In summary, these provisions are not hidden surprises; they are calculated, legacy costs that the company’s strong cash position (€1.1 billion) can handle without any issues.

Ukraine Check Finally, a quick note on geopolitics. Some investors think Buzzi is a play on the future reconstruction of Ukraine. It isn't. They exited the country. In late 2024, they completed the sale of their Ukrainian assets to CRH (Cement Roadstone Holdings) for roughly €100 million. Management preferred to take the cash and de-risk the balance sheet immediately rather than wait for a potential post-war boom. So, if the country gets rebuilt, CRH will sell the cement, not Buzzi. The "reconstruction premium" does not exist here.

4. Capital Allocation & Management

The Buzzi family runs the show here through Fimedi SpA. They hold the majority of voting rights, so let’s be clear: minority shareholders are just passengers. The family’s wealth is completely tied to the firm’s survival, which aligns them on risk management but not necessarily on maximizing the stock price next week.

This ownership structure explains the massive inefficiency in the balance sheet. The preliminary 2025 results show a Net Cash position of €1,131 million. Critics are right to point out that holding over €1 billion in the bank earning 3-4% interest, while the cement business yields significantly more, destroys value mathematically. It drags down the Return on Equity (ROE). However, if you are expecting a sudden special dividend to fix this, don’t hold your breath. This excess liquidity is their insurance policy. They are willing to accept a lower return on equity to ensure zero bankruptcy risk. As an investor, you have to accept that you are paying for a floor, not a catalyst.

Buyback activity tells the real story. In the first half of 2024, they spent €52.5 million on buybacks. But throughout 2025, even as the cash pile grew by nearly €400 million, activity dropped significantly. Management is signaling that they prefer hoarding liquidity over returning it to us. When insiders with over €1 billion in the bank stop buying their own shares at these low multiples, it confirms they are conservative, not opportunistic.

Strategic Doubts: The Brazil Move This conservatism contrasts with their aggressive move in Brazil, where they acquired 100% of Nacional Cimentos. Financially, this looks like a step back. They are using cash generated in hard currency (Dollars/Euros) to buy assets in a volatile soft currency (Real). They are also trading the group’s average margin (27%) for a lower-margin business (21%). So, why do it? It’s a Demographic Arbitrage. Europe is shrinking and the US is growing slowly, but Brazil is expanding. Buzzi is trading current margin quality for future volume. It’s a long-duration hedge against European stagnation, securing the sheer tons needed to keep the group relevant in 2040.

On the positive side, the capital structure is clean. Buzzi doesn’t use stock options. While many US industrial firms print new shares to pay executives (diluting you every year), Buzzi pays bonuses in cash. The financial statements confirm “no dilutive instruments.”

Note: You might see “Put/Call Options” in the annual report. Don’t confuse these with salary. Those are financial derivatives related to the buyout of the remaining stake in the Brazilian operations (Nacional Cimentos), not executive compensation. They treat equity as sacred, not as currency to pay the staff.

I usually skip ESG sections because they are often just marketing, but here it actually determines the CEO’s paycheck.

Safety equals uptime: Short-term bonuses depend on safety records. In this industry, a serious accident means regulators shut the plant down. If the kiln isn’t burning, cash flow stops.

The Carbon Hedge: They put 30% of their variable pay on the line to hit CO2 reduction targets by 2026. Management is effectively hedging the regulatory risk with their own bank accounts.

To summarize, management is prudent, disciplined, and painfully conservative. They refuse to dilute shareholders, which is great, but they also refuse to return the massive cash pile. You are investing in a bunker managed by people who play defense first, offense second.

5. Financial Analysis: The Margin Check

We need to view 2024 as the exception, not the baseline. The company delivered record margins back then, which was the peak of the cycle. The full-year 2025 data confirms the reversal. The operating leverage that drove profit growth for years has stalled because fixed costs remain high while the top line is flat or declining in key regions.

The Numbers (FY 2025 Update)

Recurring EBITDA: €1,230 million (Top of guidance).

Trend: On a like-for-like basis, EBITDA dropped around 6%.

Shift: Management has adapted. In the US, prices actually declined slightly in the final months. They are prioritizing volume retention to cover fixed costs. The “super-cycle” of infinite pricing power has officially ended.

5.1 Regional Performance

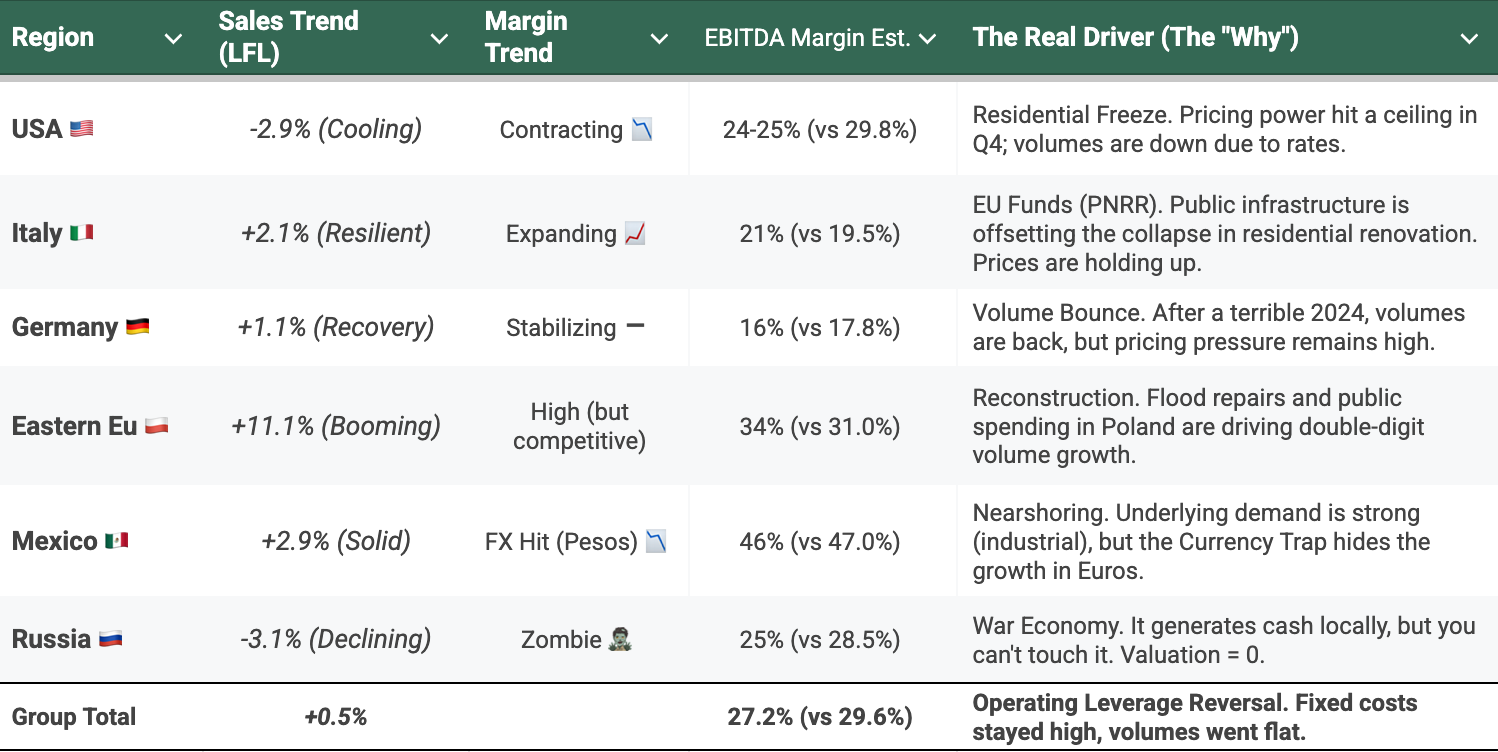

Consolidated numbers hide the truth. To understand the risk, we have to slice the EBITDA by geography. The story of 2025 is a divergence between a cooling US and a stabilizing Europe, all distorted by massive currency swings.

In 2024, the US was the margin king (30%). In 2025, the US margin collapsed to 25%, while Europe (Italy/Poland) expanded. The "Safety" of the group now relies on Europe holding the line while the US digests the high-interest rate cycle. The Group Margin erosion (240 basis points) is the price paid for the US slowdown.

A. USA: Cooling Down This is the most critical datapoint. The US represents the bulk of the profit, and the growth story has paused.

Data: Sales fell 7.0% (or -2.9% without the currency effect).

High interest rates froze the residential sector. While infrastructure spending (IIJA) is there, inflation eroded the real volume of projects.

Management Signal: Prices declined slightly in Q4. They are pivoting to defense. The goal now is to protect market share. The pricing power “party” is over for now.

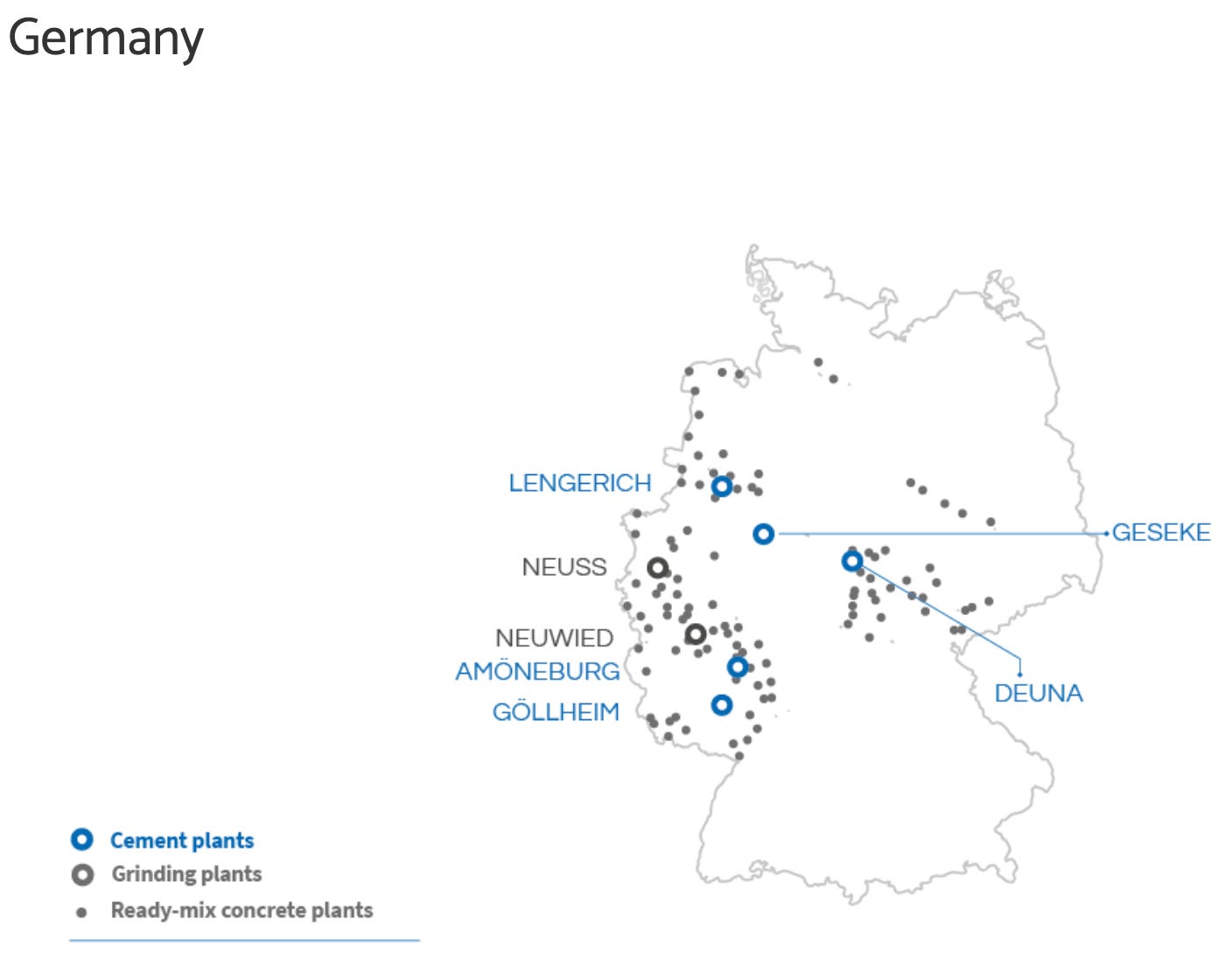

B. Central Europe: Recovery Germany and Benelux are no longer the drag they were in H1.

Germany Dat: Sales actually rose 1.1%. Volumes recovered after a terrible start to the year. The “hedging mistake” (high electricity costs locked in previously) is rolling off, allowing margins to stabilize.

Benelux: Strong growth (+7.5% sales) driven by infrastructure projects. Europe is proving to be a stable floor for the group, even if it’s not a high-growth engine.

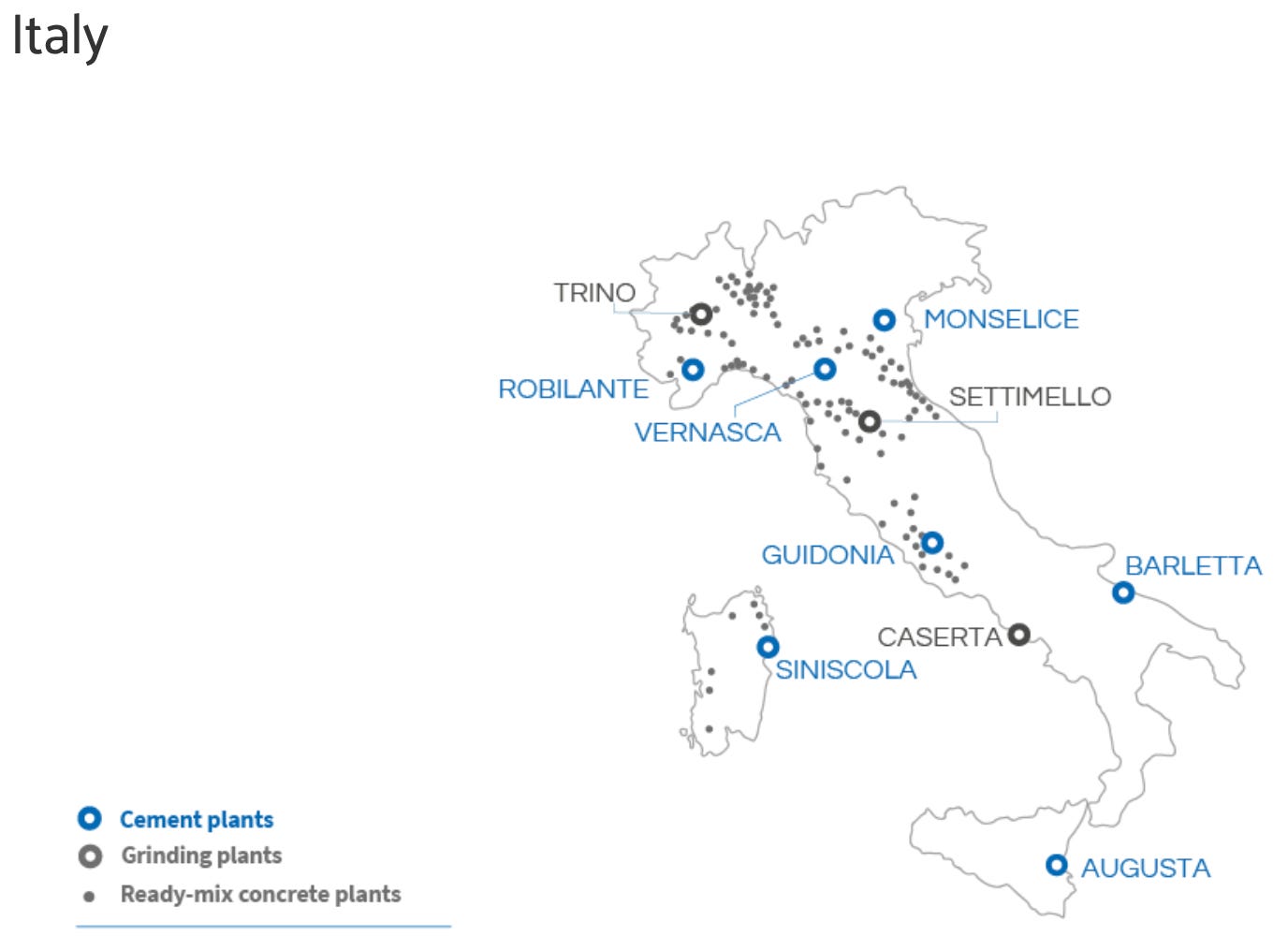

C. Italy: Resilient thanks to PNRR The headline numbers show a drop (-3.3%), but this is misleading due to the sale of the Fanna plant.

Data: Like-for-like sales actually grew 2.1%.

The Driver: The massive inflow of EU funds (PNRR) for infrastructure is keeping volumes alive despite the collapse in residential construction (end of “Superbonus”). Prices here showed a positive trend, unlike in the US.

D. Eastern Europe: The Growth Engine Poland continues to be the surprise savior.

Data: Sales jumped 12.8%.

Strong demand from infrastructure and flood reconstruction efforts. This region is acting as a counter-cyclical hedge, offsetting the weakness in the West.

Note on Russia: The assets are still running, but we must treat this as “Zombie Capital.” It generates cash locally, but the risk of expropriation makes it irrelevant for valuation.

E. Latin America: The Currency Trap Operationally, Mexico is a beast. But the financials are messy due to FX.

Data: Reported sales fell 5.8%, but in constant currency, they actually grew 2.9%.

The devaluation of the Peso and the Real wiped out the operational gains when converted to Euros.

Strategy Shift: Mexico remains the group’s “cash cow,” but the strategy is shifting from pure volume to vertical integration. Through the Moctezuma JV, Buzzi is expanding its footprint in the West (aggregates/crushing).

Nearshoring: While residential is weak, the “Nearshoring” effect (factories moving from Asia to Mexico) is driving demand for industrial warehouses in the North. This is the structural hedge against political uncertainty.

Summary The group is trading high-margin US dollars for lower-margin Euros and volatile emerging market currencies. The diversification kept the ship afloat in 2025, when the US sneezed, Europe didn’t catch a cold, but the quality of the earnings mix has deteriorated compared to the peak of 2024.

5.2. The "One-Off" Defense vs. The Math

Back in the H1 earnings call, CEO Pietro Buzzi argued that the margin drop looked worse than reality due to specific, non-recurring costs. He identified about €13-15 million in unusual expenses like legal fees (€7m), a rare bad debt write-off (€3m), and higher winter maintenance (€4m).

Check (Calculated) Management claimed the performance was distorted. Let’s test that hypothesis by adding those costs back to see the underlying profitability.

The Calculation (Normalized EBITDA)

Reported EBITDA: €526 million.

Add-back (Legal): +€7 million (est).

Add-back (Bad Debt): +€3 million (est).

Add-back (Winter Maint.): +€4 million (midpoint est).

Adjusted EBITDA: €540 million.

The Result

Reported Margin: 24.1%.

Adjusted Margin: 24.7%.

H1 2024 Comparison: 26.7%.

Management claimed the performance was distorted, but let's test that hypothesis. If we add back every single excuse and every Euro (€14M total), the normalized margin was still 24.7%, which is 200 basis points lower than the previous year (26.7%). This calculation proves that the "one-offs" accounted for only a tiny fraction of the drop. The remaining 2.0% decline came from core business issues: negative operating leverage and the end of pricing power in the US. The full-year results justified our skepticism. The structural compression was real. However, we have to give them credit: despite the headwinds, they managed costs well enough in the second half to hit the top end of their guidance.

5.3 DEBT & LIQUIDITY

In an industry typically defined by heavy leverage, Buzzi is an anomaly. While competitors struggle to service debt in a high-interest environment, Buzzi holds a massive net cash position.

The preliminary data for December 2025 confirms the trend: Buzzi holds a Positive Net Financial Position of €1,131 million. This figure is critical because it grew from €755 million in Dec 2024 to €1.13 billion today. That’s a €376 million increase in a single year, even while absorbing acquisitions.

The Bond Cancellation Signal The most telling detail in the February report is a single sentence: “The company decided not to proceed with the bond issuance approved in August.”

This confirms our thesis on their debt strategy. Management faced a choice:

Refinance at historically high rates, locking in expensive interest payments for the next decade.

Pay it off with cash and rely on internal resources.

They chose the second option. By cancelling the bond, they are telling the market: “We don’t need your money.” They prefer using their own cash rather than committing to a high fixed coupon for years. It buys them flexibility.

In 2015, the company had a Net Debt/EBITDA ratio of 2.2x. Today, that ratio is negative. This was a deliberate, decade-long process of deleveraging that culminated in an S&P rating upgrade to BBB+ (Stable) in June 2025.

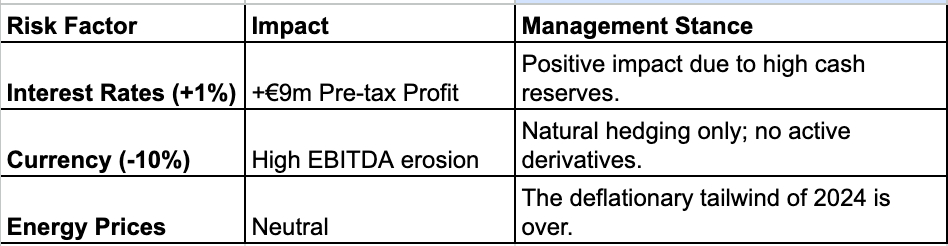

“Natural Hedge” Because Buzzi holds more cash than debt, the interest rate environment is effectively neutral for them. While the variable cost of their gross debt has risen (to 4.33%), they earn significantly higher interest income on the €1.1 billion sitting in their accounts. This setup acts as a natural hedge. If rates drop in 2026, their interest expense falls immediately. By staying liquid and variable, they are not trapped in expensive long-term paper.

Conclusion Buzzi’s balance sheet is immune to the credit cycle. The rising cost of gross debt is irrelevant because their cash reserves exceed their obligations. They have the financial freedom to ignore volatility, but, as noted in the Capital Allocation section, the question remains: When will they actually spend it?

5.4. CASH FLOW: The Green Tax

We look at cash generation, not just accounting profit. And here is where we need to be very careful. Historically, Buzzi converted a high percentage of EBITDA into Free Cash Flow. But looking ahead, that era is ending. We are watching a structural shift in how this company spends money.

The numbers show a clear trend change. In 2023, industrial CAPEX was €303 million. In 2024, it rose to €448 million. The 2025 data confirms this is the new baseline. Investors need to understand the nature of this spending. It isn’t growth; it’s the cost of the “License to Operate.” They are studying carbon capture projects (CCUS) that cost €50-100 million per year. The CEO admitted the financial return is hard to justify at current carbon prices. However, without this technology, the plant might become obsolete after 2040. It is effectively a tax to stay in business. The €350M+ annual spend going forward doesn’t necessarily add new tons of capacity or sales. It simply replaces old kilns with electric or efficient ones.

This leads to an uncomfortable question regarding the multiple. A 6x EBITDA today is “more expensive” than a 6x EBITDA five years ago because the cash conversion is worse. The bottom line is that Buzzi is hoarding cash today to pay for survival tomorrow. The €1,131 million on the balance sheet isn’t “surplus” cash waiting to be distributed to us. In management’s view, that money is already committed to the industrial upgrade. It’s a reserve for the next 5 years of mandatory spending, not a war chest for dividends. This explains the lack of buybacks. They are prioritizing the longevity of the family business over the short-term gratification of the share price.

5.5 M&A STRATEGY: Portfolio Reconfiguration

The period 2024-2025 marked a significant shift in the group’s structure. Management didn’t just sit on their hands; they executed four major transactions to alter the geographic risk profile and secure supply lines.

1. Brazil: Full Consolidation Buzzi moved from a 50% Joint Venture to owning 100% of Nacional Cimentos.

Cost: They paid €301.8 million for the remaining half, plus roughly €67 million for the ETP subsidiary.

Brazil provides the demographic growth that Europe lacks. Consolidating the business adds significant sales volume, but it comes at a cost to the margin profile. Brazil runs at a 21% margin versus the group average of 27%.

Result: It’s a margin-dilutive move that increases exposure to the volatile Real (BRL), but it secures a dominant position in an emerging market without building new capacity from scratch.

2. UAE: Vertical Integration (Gulf Cement) They acquired a controlling 57.6% stake in Gulf Cement Company (Ras Al Khaimah).

Price: The purchase price was significantly below book value, generating a “Badwill” (Negative Goodwill) gain. This is classic Buzzi: buying assets for cents on the dollar.

This isn’t just a play on the local Dubai market. It’s a strategic supply move. Buzzi intends to use this plant to produce low-cost clinker and export it. It effectively acts as a hedge for their US operations, potentially replacing third-party imports with their own production.

3. The Exits (De-risking)

Italy (Fanna Plant): They swapped an operational plant in Italy for a 25% financial stake in Alpacem (Austria). They traded active operational headaches in a difficult market for passive equity income. Smart move.

Ukraine: The report confirms they have effectively deconsolidated/sold the assets to limit exposure. It removes the operational risk of the war zone from the portfolio.

Investors need to read the 2025 consolidated figures carefully. The headline numbers lie.

Inorganic Growth: The reported sales increase of +4.8% was driven almost entirely by these acquisitions. On a like-for-like basis (organic), growth was a flat +0.5%. The legacy business is stagnant; the growth is bought.

Here is the most impressive stat of the year. Despite spending nearly €400 million on these transactions (Brazil + UAE), Buzzi still increased its Net Cash position to €1,131 million. They funded a massive portfolio transformation entirely with internal cash flow and still ended the year with more money in the bank than they started with.

Conclusion Management is rotating capital from stagnant markets (Italy) to growth markets (Brazil) and logistic hubs (UAE). The Gulf Cement deal is particularly notable; it turns a standalone acquisition into a cost hedge for the US division. This is industrial logic, not financial engineering.

6. RISK ASSESSMENT: Operational & Macro Headwinds

While the balance sheet protects the company from a liquidity crisis, it doesn't protect the P&L from volatility. Buzzi is facing a convergence of negative macro trends, and the biggest one is strategic.

6.1 US Demand: Negative Operating Leverage The US has been the group’s profit engine for years, effectively printing money. Now, that engine is officially sputtering. Management previously blamed the weather, but the full-year data confirms a structural slowdown.

Sales in the US dropped 7.0% in 2025.

High rates have frozen housing starts. While infrastructure funding (IIJA) is there, inflation eroded the purchasing power. Budgets buy less material than projected three years ago, causing project delays.

The immediate risk is Negative Operating Leverage. When volumes drop, margins contract faster than sales. Cement plants have massive fixed costs. You can’t fire half the kiln staff just because volume drops 7%. Every lost ton hurts the bottom line directly. As we saw in 2025, if the US sneezes, the group margin compresses.

6.2 Strategy: Diversification or “Empire Building”? This leads to the strategic doubt regarding the recent expansion in Brazil. We are seeing a shift in the asset mix.

Buzzi is using cash generated in hard currency (Dollars/Euros) to buy assets in soft currency markets (Brazil).

Dilution: Brazilian assets historically have lower margins and higher volatility than the US business.

Is this smart long-term diversification to reduce dependence on the US? Or is it just “Empire Building”, growing the size of the company for the sake of it, while sacrificing Return on Invested Capital (ROIC)? By swapping US exposure for Brazil, the company becomes larger but potentially less profitable and more volatile.

6.3 Currency Exposure: Buzzi reports in Euros, but the cash is generated in Dollars, Pesos, and Reals. With the full consolidation of Brazil, the earnings quality is changing.

The February report states that foreign exchange rate changes negatively impacted revenues by €50.7 million.

Mexico Trap: Look at Mexico. Operationally, sales grew +2.9%. But because the Peso devalued, reported sales in Euros fell 5.8%. The currency wiped out all the operational gains and then some.

No Hedging: Management relies on “natural hedging” (matching local costs with local revenue). This protects the local subsidiary’s cash flow but leaves the consolidated Euro results fully exposed to these swings.

6.4 Russian Assets (Stranded Capital) The Russian division remains a valuation headache.

Status: It generated €303 million in sales in 2025, but Buzzi has zero operational control. It is effectively stranded.

Risk: The risk of expropriation is higher today than ever. As long as these assets remain on the books, many institutional investors (ESG mandates) are barred from owning the stock. This creates a permanent ceiling on the valuation multiple.

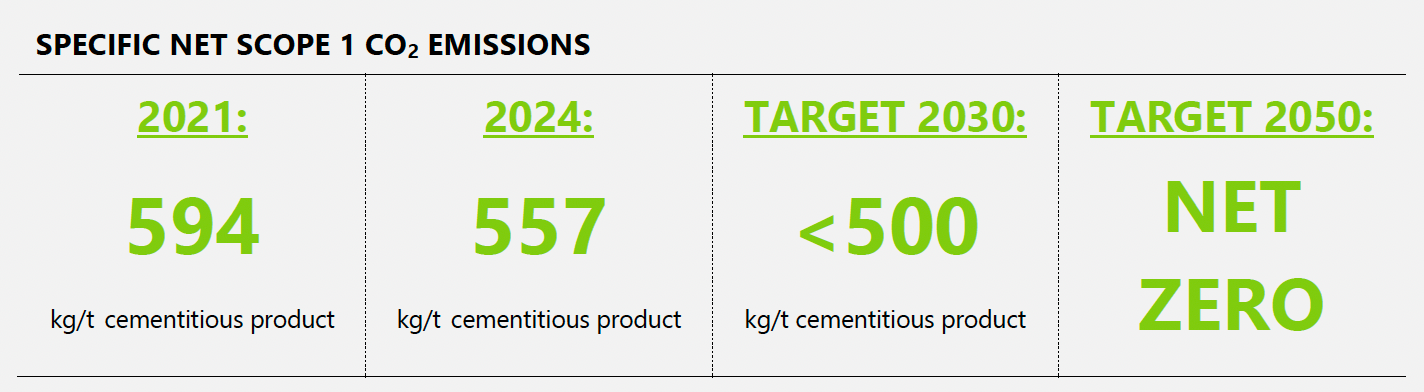

6.5 Regulatory Risk: The CBAM Test The transition to a low-carbon model is the primary long-term threat. Free CO2 allowances in the EU will disappear by 2030. Eventually, Buzzi will pay for every ton emitted.

The wildcard is the Carbon Border Adjustment Mechanism (CBAM). It’s designed to tax imports from countries with lax environmental laws (like Turkey or North Africa).

Risk: The mechanism is untested. If CBAM fails to effectively penalize these imports by 2026, European plants will become uncompetitive due to their higher carbon costs compared to non-EU rivals.

Summary Buzzi faces an operational squeeze, not a financial one. The “easy money” era in the US is over. We are trading high-margin US growth for lower-margin Emerging Market volatility. The risk isn’t bankruptcy; it’s a prolonged period of margin compression where the company gets bigger (in revenue), but the profits stay flat.

6.6 Financial Sensitivities

7. VALUATION: The Model

We have rebuilt the model to reflect the new reality: higher capital requirements ("Green Tax") and a structurally lower margin profile due to the Brazil integration. We are no longer betting on a massive re-rating; we are pricing in the inefficiency.

Assumptions (Feb 2026)

Entry Price: <€48.00 (Current Market Cap €8.6B).

Net Cash: €1,131M (Starting point).

The “Green” Discount: We have permanently lowered the target multiples to account for lower Free Cash Flow conversion.

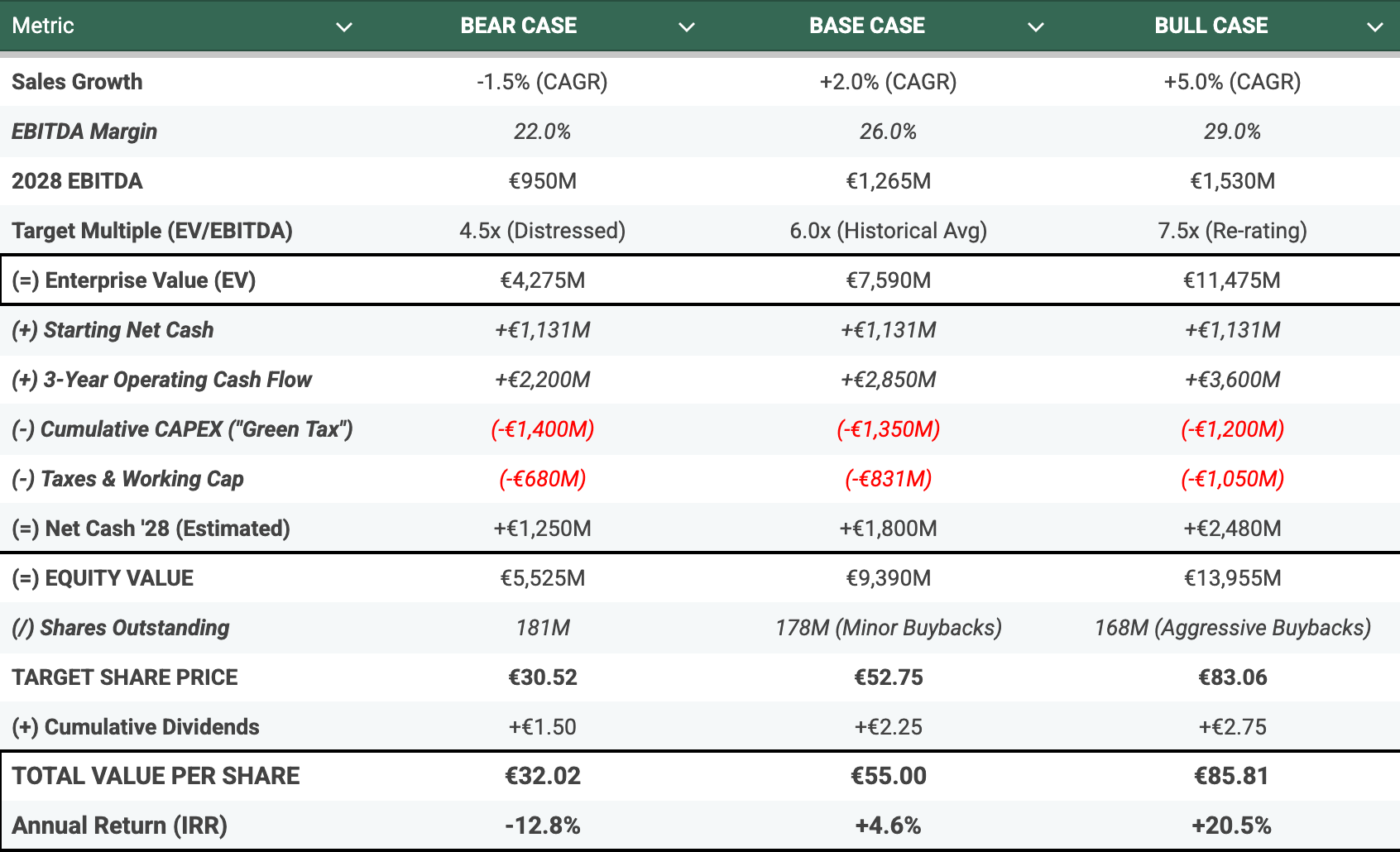

7.1 Scenarios (2028 Projections)

7.2 Scenario Analysis

We didn’t want to overcomplicate the model with endless variables. Instead, we defined three industrial realities based on how the sector actually works.

Bear Case Yes, I asume a hostile environment where everything goes wrong. We project a recession in residential construction (-1.5% sales), which hurts margins significantly due to operating leverage, dropping to 21.5%. But the critical part is the Capex. In this scenario, we assume decarbonization remains expensive, inflation persists, and no public subsidies arrive. Buzzi still has to pay the full €1.5B bill just to keep its license to operate. It’s a mandatory cost with no financial help. The market prices this distress at 4.5x EBITDA.

Base Case This is a projection of the current trend. Sales stay flat (+2%), driven mostly by inflation rather than volume. Profitability remains stable at 25.5% because the operations in Brazil and Mexico compensate for the weakness in Europe. We apply a 6.0x multiple, which is simply the historical average. You pay a fair price for a stable business.

Bull CaseThis is where the US assets finally shine. We assume the federal infrastructure funds (IIJA) turn into real cement demand, pushing sales up by 5.0%. With US plants running at full capacity, margins expand to 28.0%. Here, the “Green Tax” drops to €1.2B. We assume Buzzi executes efficiently and, crucially, receives EU or US subsidies to offset the cost. The market stops seeing it as a boring Italian company and re-rates it to 7.5x, closer to its American peers.

7.3 My Verdict

The math suggests the margin of safety changes significantly depending on the entry price. After factoring in the “Green Tax” and the management’s conservative approach, here is how the risk looks:

Price below €42: At this level, the discount on the US assets is wide enough to cover the “lazy” balance sheet and the mandatory carbon costs. The risk/reward starts to look asymmetric.

Price between €45 and €50: The company acts more like a bond. It’s stable, but the annual return in a normal scenario (Base Case) is only ≈ 4%. You aren’t paying for growth here; you’re paying for a fortress.

Price above €52: At these levels, the “Italian Discount” is practically gone. You’re paying for a recovery or a change in governance that hasn’t happened yet.

It’s not a high-growth play. It’s an exercise in valuation. The current market price implies a specific trade-off between absolute safety and mediocre returns.

8. FINAL THOUGHTS

Let’s be crystal clear to wrap this up. Buzzi is a cement company run by a conservative Italian family that doesn’t care about the daily stock price. It isn’t AI, and it certainly isn’t “sexy.”

After stripping away the marketing and looking at the numbers, the conclusion is simple: You buy Buzzi for the floor, not the ceiling.

Asset vs. Manager You are buying prime US infrastructure assets (specifically in Texas and the Midwest) and a balance sheet with €1.1 billion in cash. The catch is that you are hiring a management team that plays defense, not offense. The Buzzi family won’t change. They will keep hoarding cash to sleep well at night, they will buy lower-margin assets in Brazil for “demographic survival,” and they will spend millions on green kilns just to stay in business. This inefficiency is the price we pay for a company built to outlast its competitors.

The “Opportunity Cost” Warning This is the most important part of the thesis. This is not a play for strong capital appreciation. If you are looking for a compounder to double your money in a normal market, look elsewhere. Buzzi makes sense only in a specific context: Fear.

If the market crashes and you need a bunker to protect your capital, this is a valid option. But in a standard bull market, the opportunity cost is just too high. Current holders are likely betting on a multiple re-rating, hoping the market suddenly wakes up to the value. That is a dangerous game with this governance structure. Sure, there is always the optionality, maybe one day the family wakes up and deploys that €1 billion into a high-return asset, changing the picture entirely. But we cannot invest based on hope.

The Verdict As it stands today, with the data we have analyzed, this is not an immediate opportunity. It is a stock to keep on the watchlist for a rainy day, not one to chase in the sunshine.

THE LAST WORD (Your Responsibility)

“The most important investment you can make is in yourself.”

I have presented the data, the risks, the valuation models, and the strategy. My goal was to analyze the balance sheet in detail to verify the management’s plan.

However, the final decision is yours.

Please do not invest based solely on this analysis. You should only consider this investment if you fully understand the business model and have the conviction to hold the stock for the long term, regardless of short-term price movements.

You've read the thesis. Now see it. 👇👇

→ https://colubeatid.github.io/Buzzi-SpA/

Future issues: the interactive presentation will be exclusive for paid subscribers.

🎯 If this thesis was helpful...

→ Leave your email below (it’s free) to receive the next value investment theses before anyone else.

→ RT + Follow for more analyses like this

→ Reply with your opinion on $BZU.MIThanks for reading to the end!

This Substack is reader-supported. To receive new posts and support my work, consider becoming a free or paid subscriber.

DISCLAIMER: Nothing in this document constitutes financial advice. I am not a financial advisor. This report is for educational and informational purposes only and represents my personal opinions and research. All investment strategies and investments involve risk of loss. You should consult with a professional financial advisor before making any specific investment decisions.